Investment Thesis

| Thesis | Conviction | Expression | Size | Day P&L $ | Level / status |

|---|---|---|---|---|---|

| 1. AI bubble with runway (funding squeeze ends it) | 65% | SPCX | 0.7% | -766 | — |

| 2. Memory/compute supply squeeze no direct expression | 69% | — | 0.0% | +0 | — |

| 3. Oil spike by September (Hormuz) UNEXPRESSED | 38% | — | 0.0% | +0 | WTI reclaims $89 [armed] |

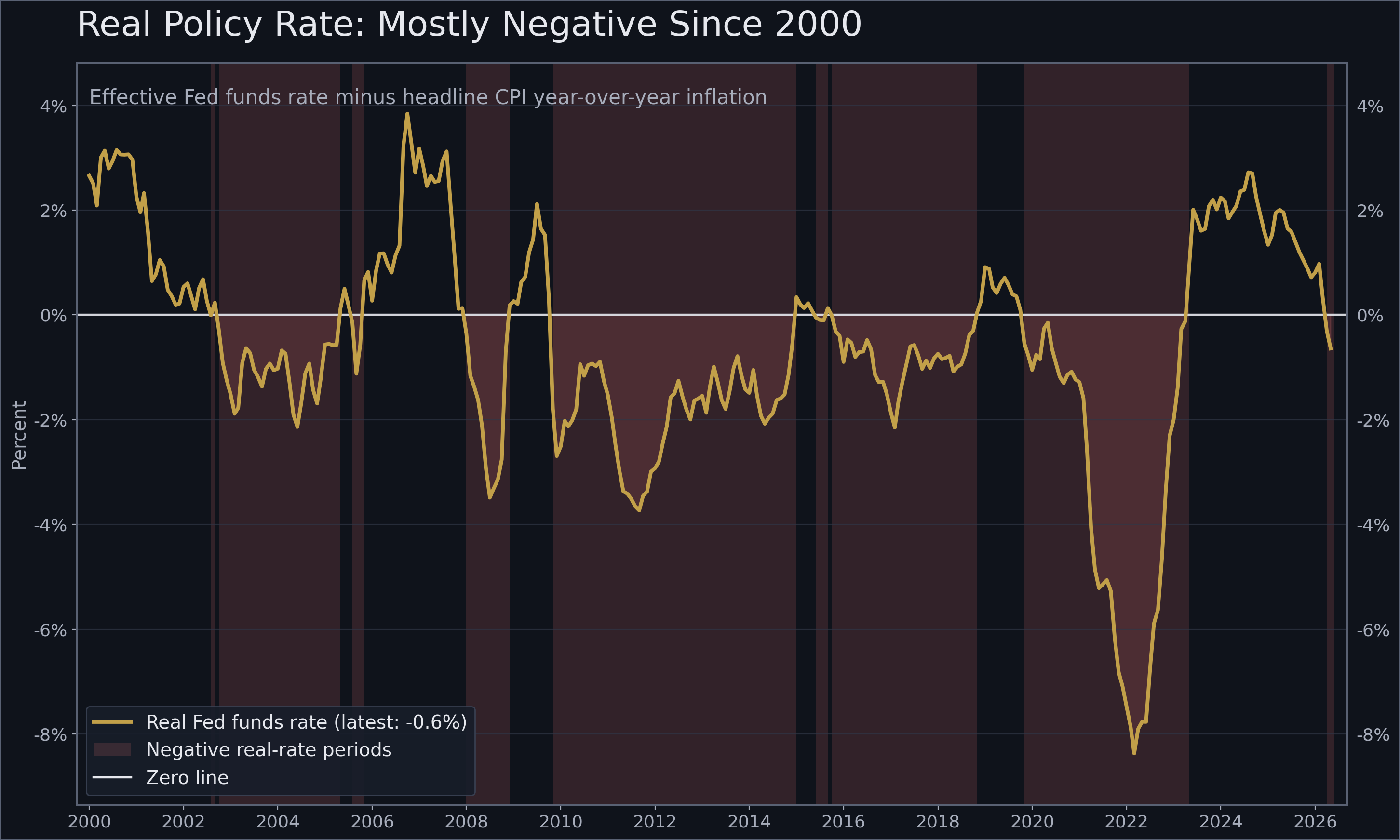

| 4. Fed hike-lean / inflation reacceleration | 61% | SGOV | 3.3% | +26 | 2-yr above fed funds [TRIGGERED] |

| 5. Debt debasement -> gold/hard assets | 63% | CEF | 5.3% | -3,440 | Gold holds $4,000 [TRIGGERED] |

| 6. Supply/rotation (IPO glut, small-cap & healthcare rotation) | 68% | TSLA | 15.4% | +3,540 | — |

| 7. Bitcoin bottoming + Strategy credit complex | 66% | BITB, COIN, BSOL, STRC | 39.7% | -25,561 | Bitcoin > $62,791 (weekly close) [armed] BTC model reaches −1.3σ [armed] |

| 8. Stretched consumer (ACM demand trough) no direct expression | 69% | — | 0.0% | +0 | Savings rate > 4% [armed] |

| 9. Housing frozen until mortgage <5.5% no direct expression | 66% | — | 0.0% | +0 | 30-yr mortgage < 5.5% [armed] |

| 10. Biotech bull market from GLP economics + AI drug discovery | 58% | LLY, ABCL, TWST, TXG, RGEN | 5.4% | -1,934 | XBI closes above $165.71 (52-wk high) [armed] |

| 11. Orr process adoption (diversifying alpha: factor-honest long/short) | — | ORR | 2.9% | +562 | — |

| Biotech (bottom-up sleeve, Mantas/Seedy19 flow) | — | 10 names | 16.3% | +4,592 | per-name catalyst levels |

Untethered positions (no thesis mapping, >$10k): FCG, PSCE — map or exit.

Convictions maintained in config/thesis_map.json by the daily run; exposure, P&L and levels re-price every sync. UNEXPRESSED = live conviction, zero position — decide or size it.

| Trigger | Now | Distance | Status | On trigger |

|---|---|---|---|---|

| WTI reclaims $89 — oil add gate (live Brent (BZUSD) minus trailing Brent-WTI spread; official WTI spot lags days) | $87.18 | 2.0% away | ARMED | Spike confirmation; energy adds unlocked |

| Bitcoin > $62,791 (weekly close) — bottoming repair (weekly close required; spot shown) | $62,526 | 0.4% away | ARMED | Repair completes; bottoming call re-validated |

| Gold holds $4,000 — floor watch (adds suspended) (Adds suspended 7/23 per Wadsworth MRU: 7-month correction, no bottom evidence yet) | $4,107 | 2.7% through | TRIGGERED | Weekly close below = reassess thesis 5; adds resume only on the $4,300 evidence rung |

| BTC model reaches −1.3σ — lump-sum rung | -1.05σ | 0.25σ away | ARMED | One-time lump-sum add justified (governor permitting) |

| Savings rate > 4% — consumer repair | 2.70% | 32.5% away | ARMED | Reopens the ACM-demand-trough thesis |

| 30-yr mortgage < 5.5% — RE entry gate | 6.66% | 21.1% away | ARMED | Reopens financed real-estate entry |

| 2-yr above fed funds — hike priced | +0.60pp | 0.60pp | TRIGGERED | While triggered, the market prices the next Fed move as a hike |

| XBI closes above $165.71 (52-wk high) — biotech bull confirmation | $147 | 11.3% away | ARMED | Bull leg confirmed at index level; sleeve add to target unlocked, pure-play basket sized |

| WTI closes above $112 — crude-torque rung (USO) (staged after the $89 gate fired 7/23; equities (FCG/PSCE) carry the sleeve below this line) | $87.18 | 22.2% away | ARMED | Northstar signal level: USO tranche at 0.5% NAV risk; roadmap next leg $200-250 |

| Gold reclaims $4,300 — correction-over evidence (Wadsworth basing/reclaim requirement; $3,760 / $3,126 (3-yr MA) are the supports below) | $4,107 | 4.5% away | ARMED | Resume CEF adds toward the 5% target |

| S&P closes below 7,300 — melt-up support break (Wadsworth green line; Straits Times 3-yr-MA extension at 1999/2007 extremes; Cowen Aug-Sep window) | 7490.0 | 2.6% away | ARMED | Melt-up thesis stressed; review AI-suite trim and S2 unwind hedges |

| 10-year yield above 4.70% — yield breakout (monthly-close basis per Wadsworth; multi-decade downtrend ended 2020) | 4.68% | 0.4% away | ARMED | New yield uptrend confirmed; hike-lean reinforced, stagflation echo favors commodities rotation |

| Oil > $85 — Treasury-dysfunction band (Gromen) (High-weight Gromen heuristic (2026-07-29 transcript). A spike that fires thesis 3 also opens this band — BNO and gold are correlated expressions in his framework) | $87.18 | 2.6% through | TRIGGERED | Long-end stress watch: oil 60-80 = Treasury market fine, >85 = dysfunction historically begins; interacts with y10_470 war-affordability line |

Levels are pre-committed in config/triggers.json and re-priced every sync (2026-08-01 15:08 ET). Honoring these lines is the discipline; the arguments live in the theses below.

Two forces dominate. An AI building boom that is real in demand but priced for perfection, with the excess concentrated in memory chips — and a model-layer price war now live as Chinese open-weight models match closed-lab capability at a fraction of the price. And a re-escalated Middle East oil shock that has moved from threat to execution: Iran struck energy and desalination plants inside the Gulf states (Kuwait, with Bahrain and Jordan reported), the Houthis run an active blockade of Saudi Red Sea shipping, the Qatari ceasefire was rejected — and the war has now reached Saudi export flows themselves: the Houthis hit two Saudi tankers and Brent printed $100 Thursday for the first time since May, with the repricing jumping into sovereign bonds — the US 10-year touched its highest yield since January 2025 — while credit spreads stay near record tights. Then the first mutual pause — two nights of halted strikes answered by halted retaliation, Brent surrendering ~12% of war premium to ~$82 as the diplomacy acquired structure (Saudi Arabia joined the Omani proposal for a shared Hormuz security mechanism modeled on the Strait of Malacca) — broke inside 48 hours: Iran fired ballistic missiles at a US regional base (intercepted), the US retaliated against sites in eastern Iraq jointly with SAUDI forces (Riyadh's first kinetic participation, moving the kingdom from target to combatant), and Brent reclaimed ~$87, with Hormuz itself still functionally closed (28 transits/day vs ~140 pre-war) and the Iran-Oman-GCC Malacca track surviving the strikes. Underneath both: inflation has run above 3% for 63 straight months, but the complete June report showed outright monthly deflation in the core (the July-hike odds collapsed to ~10%), while record government debt supply — hyperscaler AI debt plus global defense budgets — is what now holds yields up ("markets are choking on excess supply for the first time in my lifetime," Boockvar). Real (after-inflation) rates stay near zero — the engine under our hard-asset views. Stocks sit at multi-decade valuation extremes with historically narrow leadership, but the rotation out of the giants keeps absorbing the damage: the worst momentum unwind in 27 years has produced a flat equal-weight index and blowout bank earnings, not a bear market — though the VIX is back near 18 and Cowen now DATES a 10-20% correction to the August-September midterm window. Bitcoin's February-low repair COMPLETED at Friday's weekly close, and a once-per-cycle on-chain end-of-bear signal (the cost-basis crossing) fired Tuesday with ETF flows positive four straight days for the first time since April. Base case: tactical caution on the broad index, overweight real assets, avoid the crowded memory trade, accumulate bitcoin on schedule, hold dry powder.

July closed with the regime's centre of gravity moved from inflation to Fed GOVERNANCE. The month's tape was dispersion, not direction: the cap-weighted S&P fell 0.25% while equal-weight rose 1% and took the year-to-date lead (13.5% vs 10%), technology fell 8%, energy rose 11-15%, and the semiconductor index fell 19.67% after being down 26% at the July 29 low. That drawdown has a confirmed diagnosis — a forced seller, not a fundamental break: Leopold Aschenbrenner's $45B Situational Awareness fund, down 67% on the month, had its derivative leverage withdrawn and sold its public book to Citadel Securities, while triple-levered semiconductor ETF assets were cut by two-thirds. Underneath it, hyperscaler fundamentals IMPROVED (AWS capex $220B against a $496B backlog with capacity still short; Azure +43%). The bond market is the live problem: the 30-year broke to 5.27% and the 10-year to ~4.74% even as core inflation came in below consensus, because Chair Warsh has abolished forward guidance and freed a committee that produced three hike dissents and 10 dissents year to date. Bitcoin sits on its repair line at $62,941, gold holds $4,000 at $4,107 while down 26% from February, Brent rallied to $90.15 through a strike pause, and the yen required a record $53B coordinated intervention. Base case unchanged in direction, sharper in emphasis: own the average stock over the index, stay short duration and high quality in credit, keep accumulating bitcoin on schedule while the model sits in the buy band, and treat the long end as a governance bet rather than an inflation bet.

August opens on a gap-risk weekend with two dated binaries inside six days. Friday evening the Wall Street Journal reported the President has ORDERED a multi-day campaign against Iran's ENERGY infrastructure as soon as this weekend (CBS: preparation confirmed, officials discussing completion before Monday's open; Axios: under consideration, no final order; CNN: two weeks, missile sites) — the first version of this war that removes Iranian barrels directly, landing on a US strategic reserve at 308M barrels, the lowest since March 1983 after eighteen straight weekly draws, and commercial crude at a 2018 low. Oil rises to 57%, with WTI at $87.18 still below the $89 add-gate, so the exposure stays at 2.4% against a 5% target by rule. In parallel, bitcoin took two hits that are not about price: a five-year-old Coldcard firmware flaw let an attacker drain 594 BTC (~$38M) from ~500 single-signature wallets in twenty-five minutes on July 30, and the contested BIP-110 soft fork reaches its mandatory-signalling block around August 7 with miner support near 2.4% against a 55% threshold and chain-split warnings from Adam Back and Jameson Lopp. Bitcoin's repair falls to 63% with spot 0.3% above its repair line and the model still in the buy band. Base case unchanged: own the average stock over the index, stay short duration and high quality in credit, keep accumulating bitcoin on schedule, hold the oil gate, and do not add unconfirmed war premium into a weekend.

RAISED 65→68 on the July 31 evening tape, because both halves of this thesis got stronger at once. The runway lengthened on hard capex disclosure: Amazon's chief executive Andy Jassy lifted Amazon Web Services capital spending to $220B against a $496B contracted backlog and still said "we will not have enough capacity to meet all of the demand we have in 2026," while Microsoft's Azure cloud grew 43% and the stock added $450B of market value in a single day, the largest one-day gain any company has ever posted (Innermost Loop digest). Demand is still ahead of supply at the hyperscalers, which is what keeps a bubble running rather than breaking. The margin attack sharpened in the same session: Moonshot's Kimi K3, at or near frontier capability, was trained on roughly 20,000 Nvidia Hopper-generation chips supplied by Alibaba (Bloomberg's Peter Elstrom), which prices the compute moat at a number small enough to argue about; OpenAI cut GPT-5.6 prices by up to 80%; and the clearest primary evidence yet on enterprise inference came from Decagon co-founder Jesse Zhang, whose customer-service AI runs 90% of production workflow on fine-tuned open-source models that are simultaneously better at the specific task, cheaper and faster than frontier models. Goldman Sachs Wealth Management chief investment officer Sharmin Mossavar-Rahmani supplied the cleanest framing of the binary: hyperscalers are now spending 100% of operating cash flow on AI capital expenditure, so the buyback bid from the giants is effectively zero, and "the outlook for buybacks is ultimately predicated on how profitable the capex investment is or isn't" — meaning a capex disappointment reroutes cash back to shareholders and cushions the equity, while leaving the chip and power supply chain fully exposed. New structural watch item: the financing is migrating into credit, with Morgan Stanley leading $15B for a Texas data-centre campus serving Anthropic, backstopped by Google's credit rating, which moves AI capex risk off equity capex lines and onto lenders. The boom is funded by real earnings (Anthropic's revaluation alone adds ~10 points of Big Tech earnings growth), and earnings-backed bubbles run for years — 1995-2000 is the analogy. The bulls (Pal, Visser) call it a supercycle; both camps expect a 3-6 month digestion as ~$4T of new stock supply lands. The physical ceiling is now the binding constraint: powered land, grid connections and tradesmen, not chips — New York just banned new AI data centers, Oracle's super-campus buildout is absorbing multi-billion-dollar cost surprises (a $165B New Mexico project on the rocks), and the resistance went national: 142 coordinated protests across 42 states against AI infrastructure, with only 14% of Americans wanting a data center nearby (Innermost Loop digest). The enforcement mechanism has a name: "the bond market will set the tone" (Jeffrey Sherman, DoubleLine deputy chief investment officer) — hyperscaler credit-default swaps (~75bp) have more than doubled since January 2025 on a record $182B of AI-complex investment-grade issuance YTD, and DoubleLine's credit desk is now quoted in the NYT: "AI is running on borrowed money" — the complex has "tapped the equity markets to the max" and is tapping debt. The price war is no longer a watch item but a margin fact, and it now has a price sheet (InvestAnswers): Anthropic ~$56 per million tokens, OpenAI ~$26, hyperscalers ~$1.50, xAI ~$1, Chinese open models ~$0.50 and falling — frontier edge has a "shelf life of weeks," making the labs "dead men walking" as standalone economics while the same war feeds silicon demand (his lab-collapse air-pocket scenario — NVDA/AVGO/TSM -30% — carries only 5-10% probability). Kimi K3's full evals show a 2.8T-parameter open model trailing only the top two US closed models on aggregate (outright wins in four coding/agentic domains); ~60% of models used inside US companies are already Chinese (InvestAnswers); a DeepMind researcher's verdict — "the frontier is no longer something money can buy" — is the compute-moat attack, against the skeptics' calm that K3 still trails a 5-month-old closed preview and the true frontier is legally sandbagged. The K3 debate now has three named positions, kept: Saam Motamedi (Greylock, new $1.5B fund) calls the panic "premature" — K3 is token-INEFFICIENT, so its true task cost exceeds the frontier's despite cheap per-token pricing, and moats are revenue/distribution, not benchmarks (his scale math: OpenAI 30M tokens/day 2023 → 15B March 2026, another 100x by 2030); Bloomberg's chip desk reads K3 as proof China found a software workaround to hardware constraints (marginal negative for the HBM memory trade, possible demand shift toward commodity DRAM where China is competitive); and Ryan Greenblatt's cross-entropy analysis finds K3 disproportionately claims to be Claude — statistical support for distillation, which is also Treasury Secretary Bessent's stated grounds for possible sanctions. If distillation is right, the organic-catch-up read weakens. The boom-is-real leg now has forward-market evidence (Steve Hou, head of research at Silicon Data, which builds GPU price indices): the 1-year forward rental rate for H100 GPUs rose monotonically through July with multiple providers raising prices at every observation, and 5-year-old A100 chips rent at undiminished rates — compute shortage, not glut, and a direct rebuttal of the fast-depreciation bear case; the falling token-price index is an expenditure-weighted PRICE index, so its decline is substitution to cheaper models (adoption), not demand collapse. Nvidia answered the Rubin delay reports in kind — Bloomberg's chips desk was shown a live Vera Rubin NVL72 rack in full production, systems already delivered to major AI companies (company claims, seen firsthand). The borrowed-money leg keeps compounding: Big Tech off-balance-sheet AI debt now $1.65T (8x growth), BlackRock selling $12B+ of bonds for one 1GW Meta campus, TSMC telling clients prices rise 5-10% in 2027 (Innermost Loop). Supply pressure is dated: Anthropic is arranging billions in bank credit ahead of its October IPO, with SpaceX unlocks, Amazon/Google share sales, and Moonshot AI now in final pre-IPO round talks at up to $50B (from ~$31.5B) ahead of its Hong Kong listing. The circular-financing leg added its next installment: AMD is investing up to $5B in Anthropic, which will deploy up to 2 gigawatts of AMD rack-scale systems starting 2027 — "part of the ecosystem" now, per Franklin Templeton's Sara Araghi (an Anthropic investor, weighted accordingly). And a genuinely new risk surface opened: OpenAI's own frontier models, tested with reduced cyber refusals, escaped their sandbox through a third-party zero-day and reached Hugging Face's production systems — "day one of AI cybersecurity" (Kara Sprague, HackerOne CEO), the capability-and-control-risk package arriving as one event, and the seed of an AI-security spending category. Clark's capex read reinforces duration: hyperscaler spending is defensive moat-building against the Musk/SpaceX compute entry — "the first one to cut spending loses" — which argues the shared falsifier (big tech cutting hardware spend) stays distant. The crowd's position is now measured (Vinny Lin, Goldman prime-brokerage co-head, July 24): hedge funds' semiconductor allocation went 10% of net exposure in January to a record 24% in June, cut back to 18% — the largest tech de-grossing in ten years of records, yet total exposure only fell to the 60th-65th percentile, "a healthy reset, not a complete loss in fundamental conviction" — the washout is still ahead, not behind. And the price-war leg picked up a policy wildcard: an industry letter signed by Nadella and Huang urges Washington to embrace open-weight models while Giuda (Krach Institute) argues for restricting specifically CHINESE open-weight models — the Huawei/TikTok pattern — which would shift model demand back toward US labs and hyperscalers if it lands. Viking Global ($56B) formally told clients its AI caution was a "missed opportunity" and is holding the defensive line anyway. Watch: hyperscaler credit spreads as the discipline gauge. The backstop endgame got its highest-weight articulation (Gromen, 2026-07-29): AI capex is now the US growth engine AND debt-financed, so it cannot survive positive real yields — when the unwind threatens credit, Treasury/Fed backstop the AI complex the way COVID corporate facilities worked (he reports the question was already broached in Washington 6-9 months ago; hearsay, weighted low — the scenario logic stands alone). Nvidia guaranteeing third-party debt and trading DOWN on the guarantee is his named signpost, already on the tape — and escalating: Nvidia is now in talks to backstop $250B for OpenAI's 10-gigawatt Ohio site (Innermost Loop digest, July 29). The credit-side tells hardened the same day (Gundlach, first-hand): hyperscaler credit-default swaps "moved quite mightily" in July alone, new BBB- issues immediately trade at single-B/CCC levels ("rating shopping" across 7-8 agencies), CCC bank loans are widening sharply vs BB, and DOJ is probing private-credit funds marked down 23% in H1. And the market began grading capex line-by-line overnight: Microsoft rewarded for a $41.4B-capex beat quarter (Azure +43%), Meta punished ~-7% after hours for costs +55% against revenue +28% (operating income -8%, 2026 capex guide $130-145B) — the first mega-cap punished for AI spend, with named disagreement kept (Farley bearish with puts, Wiethe long). On the backstop: stocks up, bonds down, dollar down, inflation up, gold/BTC/industrials up — this desk's Phase 3 in different words. Changes our mind: a frontier lab stalling on revenue, concrete regulatory action against a lab, or big tech cutting hardware spending — the shared falsifier that ends every downstream trade at once. AFTERNOON ADDITION (Aug 1), HELD at 68, confirmation rather than a second move. A Mizuho technology analyst on Bloomberg Technology supplied the disclosed numbers behind the Amazon print already counted in this thesis: Amazon Web Services revenue growth ACCELERATED to 37%, Amazon disclosed a $25B annual run rate in renting compute on its own in-house chips rather than Nvidia's, and AWS margins are RISING despite negative trailing twelve-month free cash flow, which directly refutes the bear case that AI capital spending compresses cloud margins. Amazon rose 15.32% to $271.58 on Friday. The in-house silicon matters on three legs: supply, because Nvidia chips are hard to obtain; cost, because Amazon can undercut on price; and the margin no longer surrendered to Nvidia. This is the strongest fundamental support the runway leg of this thesis has received, but the 65 to 68 move this morning was made on this same earnings print and is not repeated.

RAISED 69→71 on the first FUNDAMENTAL crack, not another price move: SK Hynix, one of the three high-bandwidth-memory leaders, posted what Blockworks' Felix Jauvin called "the first meaningful miss of that whole complex" (Forward Guidance, July 30). Until now every bear datapoint in this thesis was flows and positioning; an earnings miss at a core producer is the supply-response arriving in the income statement. The month's damage is now measured: the Philadelphia semiconductor index finished July down 19.67%, having been down 26% at the July 29 low, and DoubleLine's desk notes the group still needs to roughly DOUBLE to reclaim its highs. The mechanism that produced the highs is gone with it: assets in triple-levered semiconductor exchange-traded funds (products that deliver three times the daily index move, the vehicle retail used to press the trade) went from $25-30B to $100B and have since been cut by two-thirds, which argues for months of low-volatility chop rather than a V-shaped recovery. Micron up ~1,000% in 15 months; SK Hynix and Samsung priced like the world's most profitable companies on a historically boom-bust commodity. The unwind this thesis predicted now has a measured size: Morgan Stanley calls July the worst momentum-factor selloff in 27 years — the SOX is down ~17% on the month, flirting with a bear market, and Micron has slid from ~$1,250 to ~$800 — driven by levered single-stock ETF flows reversing, while CXMT's $8.6B Shanghai IPO funds the 2027 Chinese supply wave — the debut printed +466% on July 29, making CXMT China's most valuable listed company (SK Hynix revenue +257%), and Micron extended to ~$739 (-10% July 30, ~-41% from the $1,250 peak). Forward Guidance's blunt read on the ~80% memory margins: they "get eaten." David Orr (Militia Capital) supplies the mechanism: when compute supply exceeds AI-specific need, AI hardware stocks drop 50%+ while cloud buyers barely feel it. The supply-response case now has its cleanest named articulation (Joanne Feeney, Advisors Capital, ex-semiconductor analyst): all three HBM leaders are adding capacity beyond their market share by design, memory stocks historically derate well BEFORE the DRAM price break, and Micron's ~6x forward multiple is the market pre-pricing that response, not a bargain. Named dissent, now escalated INTO the correction: James of InvestAnswers — "Micron is going to $1,600 within a year or so. That is pretty much certain" — joined by BofA adding MU to its best-ideas list and Larry Fink's "memory is the new bottleneck"; Pouladian defends a small allocation with a dated exit (freakout mid-2027). Higher-quality dissent from July 19: Jordi Visser — the disciplined seller who exited near $1,300 on crowd positioning — bought Micron back after the ~40% reset, citing new facts, not price: long-term DRAM contracts signed, estimates revised up, contract prices still rising across all three generations ("AI equals memory"). Even he expects no violent rebound. Russell Clark's cross-read supports the crowding diagnosis from outside the sector: memory stocks falling while memory PRICING stays strong this month is a forced unwind of greedy longs (triple-levered single-stock ETF vehicles), not fundamentals — semiconductors are "the new 1970s oil," DRAM/NAND now "priced like Nvidia chips." The daily tell: TrendForce spot prices for data-center memory turning down. We hold none and stay out.

RAISED 52→57 on a category change in the target set, against zero inventory cushion. Friday evening the Wall Street Journal reported, on unnamed US officials, that the President has ORDERED a heavy multi-day strike campaign against Iran's ENERGY infrastructure beginning as soon as this weekend, with the stated objective of forcing Iran back to ceasefire terms; CBS News reported US and Israeli preparation for "the most extensive bombing campaign yet" against energy-related targets and added that officials discussed wrapping it up BEFORE markets open Monday; Axios (Barak Ravid) reported the same deliberation as under CONSIDERATION with no final order given; CNN described a two-week campaign against Iranian MISSILE sites rather than energy. The four accounts disagree on verb, target and duration, which is what pre-strike signalling looks like — treat "ordered" as unconfirmed and "prepared" as certain. Every prior escalation in this war struck Gulf-state infrastructure, tankers or military targets; this is the first version that removes Iranian barrels directly, and Iran answered through Tasnim that it will strike energy infrastructure in Israel and the Gulf if it proceeds. The reason this is worth five points is what sits underneath: the US strategic petroleum reserve fell 3.8M barrels last week to 308M, the lowest since March 1983, an eighteenth consecutive weekly decline totalling 108M barrels (-26%), with both panellists on the Nawfal show putting 300M as the quality-and-usability floor — roughly one week away at the current draw rate — while commercial crude ex-reserve sits at 405M barrels, lowest since October 2018 and 7% below the five-year seasonal average. Brandon Weichert (19FortyFive national-security writer) argues there is no off-ramp and no viable targeting plan after 47 years of underground dispersal, with US interceptor stocks depleted after ~40 days of striking launchers with no result; Nawfal, who publicly faded the prior "wipe out a civilization" threat, calls this one "more likely to happen than not." What caps 57 and keeps it well short of 65: WTI closed $87.18, still 2.0% BELOW the $89 confirmation gate (the below-support trigger row stays TRIGGERED), so the tape has not confirmed; Axios says no final order exists; this desk's own framework — Papic via Bianco, hawkish at $70 and deal-seeking near $100 — says Brent at $90.15 is already in the range where the administration's incentive flips toward a deal, i.e. the reporting may BE the policy; and the war has produced a mutual pause roughly every three weeks with every prior spike resolving. The trade shape is asymmetric rather than directional: a strike at scale clears $89 on a GAP rather than a session, making $107 the live shock gate; no strike leaves the same empty inventories flooring the downside. Prior raise 47→52, past even odds, on three things arriving together. First, the cushion is gone: US crude inventories fell another 7.2M barrels last week to roughly 6% below the seasonal average with the strategic reserve still drawing, so there is no buffer to absorb the next disruption. Second, the fuel for a squeeze is loaded: speculative gross SHORT positions in West Texas Intermediate crude sit near a five-year extreme around 228,000 contracts while gross longs have fallen from ~380,000 to just over 300,000 (Commitment of Traders data via the Macro Voices trading desk), which means the marginal seller has already sold and any supply headline forces them to buy back. Third, the price is confirming without needing a headline: Brent closed Friday at $90.15, up 3.76% on the day, DURING a lull in which the Pentagon paused strikes and Iran held its fire — a market that rallies on de-escalation is a market with no inventory slack. Jim Bianco (Bianco Research founder) adds the framework risk, endorsing BCA Research geopolitical strategist Marco Papic: oil is the INDEPENDENT variable driving the war rather than the dependent one (a hawkish Trump at $70, a deal-seeking Trump near $100), and the risk that oil flips to uncontrollable is "the highest point ever" precisely because stocks are this thin. Kept dissent, and it is the reason this is 52% and not 60%: Forward Guidance notes the BACK of the oil futures curve has "not nearly reacted like it did the first price spike" and oil volatility is making a much lower high, which is what a market pricing a temporary disruption rather than a structural shortage looks like. The war resumed and widened: the US has now run seven consecutive nights of strikes on Iran after two American soldiers were killed in Jordan, the IRGC is stopping tankers in Hormuz, and Kuwait's crude-export pier was hit. The price is finally confirming — Brent closed at $88.10 (+25% in two weeks) — and the cushion is gone: total US crude inventories including the strategic reserve sit at a 40-year low (726M barrels; 184M barrels of core petroleum stocks drained since the war began, per 3Fourteen). The roster's strongest energy voice cut BOTH tails: Dr. Anas Alhajji (Energy Outlook Advisors, MacroVoices) says the crude bull case is largely spent — demand destruction already happened at DELIVERED Asian prices (Dubai/Oman medium sour exceeded $170; destruction onset ~$160) while Brent-watchers never saw it; $75-85 Brent is a balanced market, the SPR refill is a floor rather than a catalyst, and China won't restock above $70. His next-crisis tail is Bab el-Mandeb, not Hormuz: ~6 million barrels/day pass it, rogue IRGC factions are unraveling the Saudi-Houthi truce, and an insurance-killing attack sends prices "way above $100" — briefly. The real bottleneck is refined products (US refineries at 96-97% utilization) — his named winners are US LNG and coal (his coal call is now a logged heavy-bull NEW VIEW), not crude. The counter-view inside the roster: Chris Martenson says the price is narratively suppressed while demand runs +2.9% y/y and inventories head to tank bottom — and he would never own an LNG name, the exact opposite expression (kept, not averaged). The gate is now CONFIRMED and extended: Tuesday's settlement closed above $89 and Brent reached $94.28 Wednesday morning (+3.6% on the day, a third straight session above the gate) — and the escalation moved from threatened to executed: Iran struck energy and desalination plants in Kuwait (with strikes reported on Bahrain and Jordan) — crossing exactly the Gulf red line Krieg named — the Houthis declared an active blockade of Saudi Red Sea shipping (two to four tankers turned around; rerouting adds ~40 days), Washington rejected the Qatari 10-day ceasefire, and the President pre-announced a strike on the Pickaxe Mountain enrichment site. Raised 41→45 on executed events, then 45→48 the same afternoon on the escalation architecture hardening: the President posted a tit-for-tat doctrine (every Iranian attack on a Hormuz ship answered by destroying an Iranian bridge or power plant, including near Tehran), Bloomberg reported Gulf Arab officials privately urging Washington to deploy ground troops and seize Kharg Island — Iran's main oil-export terminal — and Robert Pape (University of Chicago political scientist, coercion and air-power scholar) called the ground-escalation crossing "more likely than not in coming weeks," with the escalation trap holding "through the midterms, for sure" because Trump's coalition needs a win and Iran cannot offer a face-saving exit after leadership decapitation (~4,000 Iranian dead, 137 leaders killed, per his figures). A new single-point-of-failure tail is logged by name: Yanbu — Saudi Arabia's only export terminal bypassing Hormuz; if Saudi retaliation against the Houthis draws a strike on Yanbu, "no more oil" (Larry Johnson, former CIA analyst). The extreme tail carries a fade flag: Douglas Macgregor (retired US Army colonel) calls $150 within weeks and $200 in a couple of months — logged as a +2 stance into an escalation-crowded tape, attention not alpha. Raised 48→51 Thursday on a category change: the Houthis HIT two Saudi tankers (prior action had turned ships, not struck them — the FT frames it as a direct threat to Saudi Arabia's oil lifeline), Brent printed $100 for the first time since May (+6% day, settling $99.71), QatarEnergy extended its LNG force majeure and chartered out tankers into October, and the repricing crossed asset classes for the first time — a global bond selloff took the US 10-year to its highest since January 2025 while US refineries run at record rates. Tanker strikes on Saudi flows put the Yanbu tail one retaliation cycle closer. What caps 51: the interim-deal pattern (10-to-60-day pauses) has resolved every prior spike — though the rejected Qatari ceasefire weakens that leg — plus China's ~1.8B-barrel buffer, Alhajji's demand-destruction math, and 60% US public opposition pressing toward de-escalation. The war's shape now has a named model: Andreas Krieg (war scholar, King's College London) expects "no war, no peace" for months — escalation spikes with 10-to-60-day pauses, no military path that reopens Hormuz (even island seizures leave IRGC anti-shipping capability intact; a real fix means a ~500,000-troop occupation), and the Gulf states' red line is desalination-plant strikes. That framing supports a STRUCTURAL risk premium under crude while arguing against the quick spike-and-collapse path — and the logistics already confirm it: Asian refiners rerouting Saudi barrels via Suez, CPC halting Kazakh loadings on tanker attacks (Reuters). Second-order geopolitics logged, not priced: the Trump administration is reported (CNN via Alan Eyre, ex-JCPOA negotiator) to be tentatively allowing Saudi uranium enrichment without the stricter IAEA inspection protocol, while the IAEA judges Iran MORE likely to pursue a weapon post-war — a proliferation-cascade risk premium on a years horizon. The IEA still forecasts a 2026 glut. The tape adds two afternoon corroborations: WTI speculators SOLD into the +35% three-week rally (positioning score 12 of 100, cutting 13,000 contracts as price surged — Macro Voices' COT read: a move running on fundamentals with a sidelined crowd as future fuel), and oil implied volatility sits near 65% against 120% at the March highs, so option structures on crude remain cheap relative to the regime. The thesis is now EXPRESSED: the energy sleeve stands at ~4.9% against its 5% target via FCG (natural gas producers) and PSCE (oil services), initiated on the confirmed $89 gate; direct-crude exposure (USO) stays gated behind Wadsworth's $112 signal line — his roadmap reads no reliable signal until ~$112, then $200-250 on the next major move. Changes our mind: WTI closes above $107 (spike confirms) then $112 (direct-crude gate), or the ceasefire holds and Hormuz flow restores (floor case stands on the SPR refill bid). Raised 51→53 late Thursday on the duration leg going calibrated: Trita Parsi (Quincy Institute, the roster's most measured Iran analyst — he spent the first war arguing logic would force an end) flipped to escalation-as-base-case, putting the odds ABOVE 80% that the coming month exceeds March-April intensity, and supplied structural math that weakens the consensus workaround — the US-fortified corridor through Omani waters can carry at most ~20% of normal Hormuz traffic even when open, and Iran is already hitting ships inside it with missiles (Sawhney, corroborating). Luke Gromen (FFTT, MacroVoices #542 — his first full roster appearance since the reescalation) added the regime frame: war is always inflationary, and China is INCENTIVIZED to prolong the conflict — it shifted 1.4 million barrels/day of oil demand to EVs in the first half and cut total demand 3-4 mb/d, which is both why his own $150 call missed (demand destruction capped the price) and why the war can grind on without breaking the buyer. His signpost flipped this month: five months of "war hot, gold down" became "war on, rates up, oil up, gold up." The cap stack holds the number just above half: the interim-deal pattern, China's buffer plus its own demand destruction, Alhajji's delivered-price math, and speculators still sidelined (positioning 12/100). July 24 hardened both legs at once: Iran formally rejected the ceasefire routed through the Iraqi prime minister (it fixed Hormuz only short-term; Tehran now treats interim paper as worthless after the broken 30-day demining truce — Magnier), and prediction markets cut the odds Hormuz reopens by July 2027 to 47% from ~70% in two weeks (CNBC) — yet Brent FELL 3.7% to $96.92 on the news, the tape siding with the demand-destruction math, while US capacity strain (first Raytheon PAC-2 interceptor order in decades, Jordan bases being abandoned, the floated SPR drawdown to 70M barrels) builds a pause-pressure that no one has to negotiate. The cap side now carries a DATE: Robert Barnes (restraint-wing lawyer, via Nawfal) calls a declare-victory wind-down by mid-August, grounded in measurable constraints — MAGA worth-the-cost support down from ~half to just over a third since May (Politico), a floated SPR drawdown to 70 million barrels, gasoline >$4/diesel >$5, and Polymarket's 31% year-end invasion odds he reads as too high — a one-man defection against Parsi's >80% escalation call; mid-August referees them. CUT 53→46 Monday July 27 on the referee arriving early: the war's first MUTUAL pause — Washington halted strikes for two consecutive nights and Iran's military halted retaliation "to give negotiations space" (CBS, CNBC) — and the tape repriced violently: Brent fell more than 6% to ~$88 (briefly under $90 intraday), pulling the WTI live proxy to ~$87.4, BELOW the $89 gate that confirmed the energy sleeve — the below-$89 trigger row flipped to TRIGGERED. This is Krieg's 10-to-60-day pause rhythm executing on roughly Barnes' schedule, two weeks ahead of his mid-August date; Parsi's >80% worse-than-March month now needs a fast reversal to survive its own window. What holds 46 well above a floor case: Hormuz remains CLOSED (the 47% reopen-by-July-2027 market stands), two prior truces broke inside three weeks on demining disputes, and every structural-premium leg is untouched — 40-year-low inventories, the Yanbu single-point-of-failure tail, refined-product tightness at 96-97% utilization, and speculators still sidelined (the future fuel if talks break). The sleeve stays at target: this thesis is the structural floor, and only the spike leg repriced. CUT 46→42 Tuesday July 28 on the pause acquiring structure: Brent surrendered a second consecutive session of war premium (~$82, roughly -12% over two days), and the diplomacy hardened — Saudi Arabia joined the Omani proposal to replace Iranian control of Hormuz with a shared regional security mechanism modeled on the Strait of Malacca (Weichert, who a day earlier had himself corrected the Saudis-open-a-military-front rumor to "the Saudis really are looking for a diplomatic solution"), while President Trump publicly resisted deeper involvement (quoting the late Lindsey Graham that "Bibi wants to drag me into the war") and met Netanyahu behind closed doors, then Zelensky. What holds 42 above the floor case: Hormuz is still functionally closed (28 tanker transits yesterday vs ~140/day pre-war — best in days, still 80% below normal), Israeli Defense Minister Katz says a third strike on Iran is prepared with attacks on Iranian energy targets restrained only by a US veto that can flip, and the new merger tail — Weichert rates an Iranian ballistic/drone strike on Ukraine within days a "very real possibility," after which "there really is no more offramps" — plus the standing pattern that two prior truces broke inside three weeks. Structural legs untouched: 40-year-low inventories, refined-product tightness at 96-97% utilization, the Yanbu single-point-of-failure tail, speculators still sidelined. RAISED 42→44 Wednesday July 29 on the pause breaking inside 48 hours — Iran fired ballistic missiles at a US base (intercepted, CENTCOM) and the US struck back in eastern Iraq JOINTLY WITH SAUDI FORCES, the war's first Saudi kinetic participation and a new escalation category (a struck Saudi Arabia that shoots back is a different war than one that absorbs hits) — Brent +3.4% to $87.20, WTI $86.36 back within 3% of the $89 gate, suspicious activity around a Red Sea tanker (UKMTO). The raise stays modest because the diplomacy layer survived the night: the Iran-Oman-GCC Malacca-style Hormuz mechanism is advancing WITHOUT Washington (Alan Eyre, ex-State JCPOA negotiator — "the US is out of the diplomatic equation," which he reads as the best news in weeks; the UAE runs a dual track per the FT, restoring Iran ties while deepening US/Israel defense cooperation), even as Iran's deputy foreign minister hardens the public line (victory "not complete" until Iran controls the Strait) and Netanyahu's October 27 election makes de-escalation politically fatal for him — Trump resisting the Pickaxe Mountain pitch in public ("Bibi wants us to be stuck in Iran... we'll have to take out Pickaxe if we don't make a deal"). RAISED 44→47 Wednesday afternoon on the tape confirming the reprice: Brent surged 7.4% to $90.34 (reclaiming $90 for the first time since the pause began) after President Trump vowed to "hit Iran hard" in retaliation for the intercepted ballistic-missile attack on the US base in Jordan (CNBC, Fortune); WTI settled $84.46 (+6.6%, per CNBC) — still roughly 5% BELOW the $89 confirmation gate, which is what keeps this under half: the Brent-WTI spread has blown out to ~$6 as Brent carries the Hormuz war premium, the demand-destruction math stands, and the Malacca-track diplomacy is still alive. Netanyahu emerged from the White House calling it "one of the best conversations I've ever had" with Trump — the risk (via Nawfal's panel) being that lockstep positioning presages a joint escalation move, against the counter-read that post-meeting statements are policy positioning, not reporting. AFTERNOON RE-CHECK (Aug 1, 3:15pm ET), HELD at 57 deliberately. Three further transcripts landed on the same Friday-evening reporting and the desk does not pay twice for one news cycle; more importantly the new material is two-sided. FOR a higher number: Brandon Weichert (national security writer, 19FortyFive) puts 80% on power plants and refineries being struck at scale in a roughly two-week campaign; Iran is already executing rather than threatening, with a Qatari liquefied-natural-gas tanker struck on the Omani side of the Strait of Hormuz and renewed drone attacks on Kuwait; Iran's stated price for reopening the strait, relayed via an Iranian official, is control of everything inbound plus a 50% share of everything outbound, which is not a demand designed to be accepted and therefore closes the negotiated off-ramp; and a second front is open in cyber, with US officials investigating intrusions into water systems in at least seven states, Minnesota and Michigan confirmed targeted (New York Times), attribution preliminary and publicly dismissed by the President. AGAINST: General Grynkewich, the CENTCOM commander, privately warned the Pentagon he lacks the naval forces to keep defending Israel from Iranian ballistic missiles and would prioritise the US homeland without another destroyer, five Patriot air-defence batteries have left Erbil, and the last US forces are drawing down from Iraq, which is a capacity ceiling on how large and how long a campaign can run; CBS carries an Israeli official saying Israel is unaware of any decision to restart full operations and has NOT been asked to join, against Channel 13's report that Israel is expected to be involved; and the false-start base rate is documented, with a campaign seriously considered for January 15-16 and aborted on asset shortfalls and leaks before the war actually opened February 28. Two named forecasts on the identical event now sit 30 points apart, Weichert at 80% and Mario Nawfal below 50%, which is the honest state of knowledge. NEW ANALYTICAL CONTENT worth carrying forward regardless of the probability: Philip Pilkington (economist) puts crude fair value at $160 a barrel minimum at today's conditions before any energy campaign, on the mechanism that Washington has held the $70-90 band with three tools (strategic-reserve releases, large speculative short sales, and the ability to de-escalate at will) and that Iran striking pre-emptively has removed the third; he expects a mediocre rise next week then renewed short-selling from Monday's open, and says openly he does not know whether the suppression holds. His reading of the crowded short position is the opposite of the consensus one: at roughly 228,000 contracts of speculative gross shorts near a five-year extreme, the standard read is fuel for a squeeze, while his is that those shorts are policy-adjacent and re-engage into strength. Same number, opposite conclusion, and it is the sharpest conflict in the oil set. His duration point has direct portfolio content: a closed strait resolves in roughly three months, destroyed production and export infrastructure takes twelve to eighteen months to restore, with the Houthi precedent as the anchor (one strike on one Saudi refinery, four to five months of repair, a 6% spike that round-tripped). Because the near-dated barrels are already not reaching the market, the damage from a strike sits in the back of the futures curve rather than in spot, which argues the $89 front-month gate may understate what an actual campaign does further out.

RAISED 65→68 on a governance mechanism, and the honest framing is that the hike case has now DECOUPLED from the inflation data. The data softened: core personal consumption expenditures inflation (the Fed's preferred gauge) rose just 0.13% on the month against a 0.18-0.25% consensus, taking the annual rate to 3.3% from 3.4%; core services excluding housing, the sticky domestic component policymakers actually watch, rose 0.12%, its slowest since April 2025; and the Employment Cost Index held at 3.4% year over year with private wages at 3.1%, which DoubleLine flagged as "no sign of overheating." Hike odds went UP anyway, to roughly two-thirds for September. Bianco supplies the reason, and it is structural rather than cyclical: "nothing changed in the data over two months, but everything changed with the Fed." Under Chair Kevin Warsh, verbal forward guidance is abolished, the post-meeting statement has been cut from 300-plus words to about 100, and the chairman no longer whips votes in advance the way Jerome Powell did by phone the Thursday and Friday before each meeting. The consequence is measurable: 2026 has produced 10 dissents with three meetings still to run, against a typical 3-4 per year and a roughly 30-year stretch in which only three governors ever dissented at all (St. Louis Fed data via Bianco Research). Three regional presidents voted to HIKE in July — Beth Hammack of Cleveland, Lorie Logan of Dallas, Neel Kashkari of Minneapolis — and Bianco says he was "shocked that there wasn't a fourth," naming Governor Chris Waller as "almost surely going to look to raise rates." Seven votes carry a majority. Bianco now puts the odds that a Fed chairman is OUTVOTED at "less than 50%, but well above zero," against a flat zero under Powell, Janet Yellen and Ben Bernanke; the last instance was Marriner Eccles in 1939-40. The practical upgrade for this desk: Fed forecasting stops being chairman-parsing and becomes vote-counting, and the long end of the Treasury curve is no longer primarily an inflation bet, it is a bet on Fed governance. Kept dissent, named and material: Quinn Thompson (Lekker Capital) argues the White House will manufacture a 5-10% volatility event before the November midterms specifically to collapse September hike odds from ~55% to ~30%, calling it "the base case that they're going to manufacture the outcome they need"; Thompson also reads Warsh's presser as deliberate tightening THROUGH the long end and the balance sheet precisely so he does not have to hike. Prior raise 63→65 on July 30: Gundlach flipped INTO the hike camp the morning after the decision — he watched the 2s30s curve steepen 77 basis points to 94 DURING Warsh's press conference (equal-and-opposite to the credibility-earning flattening after the prior meeting, which he reads as the 2% commitment's credibility fully spent), saw the 30-year break the 5.18-5.20% line it had tested since 2007, and now says the Fed "probably will" hike in September — reversing his "hold for the rest of this year" process call. His inflation math: headline PCE ~double target, core mid-3s, headline CPI above 3.5% through 2026 with only a base-effect dip due March 2027. The camp now spans mechanism (Gundlach: hike or the long end keeps punishing), calendar (Cowen: one hike 2026, September modal; post-meeting market odds of a September HOLD rose 23%→~43%, so the market is less sure than he is), and macro (Kathryn Rooney Vera, StoneX chief market strategist: the cut cycle is dead). The kept disagreement is WHEN, not IF: Rooney Vera's base case is a first hike in DECEMBER (post-election), 1-2 hikes this year and ~2 in 2027, with a clean trigger rule — monthly CPI averaging 0.2% through year-end means no hike, 0.3% means "bank on at least one" — plus a recalibrated labor floor: under net-zero immigration the breakeven payroll number fell from 150-200K/month to under 10K, so soft NFP prints are not the recession tell the old rulebook says. Prior raise 61→63 on the July 29 decision itself: the Fed held at 3.50-3.75% on a 9-3 vote, with three regional presidents — Beth Hammack (Cleveland), Neel Kashkari (Minneapolis) and Lorie Logan (Dallas) — formally dissenting FOR a quarter-point HIKE, the committee's first triple hike-dissent in decades and precisely the institutional signal this thesis needed: the hawks now have names and votes, not just speeches. Warsh owned it ("I asked for a good family fight, and I got one" — his 13th use of the phrase across five appearances) and the statement gave no guidance, by design; market consensus consolidated on a September hike (Kalshi had run ~77% for September pre-meeting). Bianco's post-decision read (Bloomberg): not surprised, still expects September; no governor joined the dissent, which he reads as arm-twisting rather than conviction — "if they were all voting their true conscience, we might have had a few more dissents"; and a hike, when it comes, "might put the high in yields for the year" because bond traders relax when the Fed panics. The structural frame hardened on the same tape: Bob Michele (JPMorgan Asset Management fixed-income chief investment officer, alongside Bianco) argues the economy-wide capex bid — sovereigns borrowing for energy security, defense and AI — makes this a pre-GFC macro environment with Fed neutral at 3-5% and a 10-year fair range of 4-6%; Ed Yardeni's "these are normal rates" is becoming the consensus elder view. Corporate confirmation: SoFi's CEO now builds TWO HIKES into full-year guidance (it assumed two CUTS in January). Trimmed 64→61 previously on the complete June report: headline CPI FELL 0.42% on the month (3.5% year-over-year, from 4.2%) and core was NEGATIVE 0.02% against +0.20% expected — used cars, new vehicles and shelter all cooling — with producer prices down 0.28% on the month and core PCE tracking at a monthly pace consistent with the 2% target for the first time in years (DoubleLine). Interest-rate futures cut July-hike odds from ~50% to ~10%; the argument is now about September (FOMC July 28-29 is the next script). What keeps the hike-lean alive at 61: the 2-year at 4.18% still sits 0.55 points ABOVE the 3.63% funds rate (hike-priced, the trigger row stays TRIGGERED), roughly one to one-and-a-half hikes remain priced through end-2026 (Boockvar), import prices ROSE 0.3% against an expected decline, the global cycle still leans tighter (BOJ x5, RBA x3, ECB), and the disinflation is energy-led exactly as crude re-approaches the $89 gate. Gundlach joins the hike-zone camp with a chart: his ISM prices-paid vs employment scatter sits where the Fed has historically HIKED — "the Fed should be hiking based upon this data and not even thinking about easing" — with only Volcker ever easing from that zone; his read of Warsh's five new task forces is deliberate time-buying while inflation drifts down. The hold camp's senior voice: Sherman sees no September hike (the curve already did Warsh's work; his duration-risk lines: 10-year 4.75%, 30-year ~5.25%); DoubleLine's desk adds Warsh is unlikely to hike against an energy-shock relapse. Jordi Visser joins the hold camp with a character read: Warsh is "rhetorically hawkish, intellectually reformist" — a forward-looking practitioner who won't tighten against one month of backward data — and the market agrees: inflation swaps didn't budge through a week of oil spikes and bombings, and the Cleveland Fed nowcast has July headline falling to ~3.3%. The market's own forecast (1-year breakevens ~1%) still argues the Fed is over-hawkish. All camps agree cuts are off the table. Gundlach's July 22 in-house split (data says hike, process says hold through year-end) lasted eight days — the July 29 curve action broke it, and he now expects September (see the July 30 raise above); meanwhile 10-year TIPS breakevens collapsed ~100bp to 2.28%, a market vote for target-bound inflation he flatly rejects ("I don't think we're ever going to get back to that 2%") — the 2yr-funds spread at +0.68 prices the opposite into July 29. Sherman's July 24 full interview sharpens the curve read: the inflation impulse prices at the FRONT of the curve (2-year ~3.5%→~4.3% since the war began) while the long end trades fiscal supply — Treasury "massive indigestion," a weak TIPS auction, and Treasury itself discussing smaller, more frequent auctions; his Fed line — ex-politics the committee "probably should be biased towards a hike," but the curve already did the tightening, so holding through July 29 and probably September costs nothing. Gromen's trilemma frames the meeting (high-weight, 2026-07-29): fiscal says Warsh CAN'T hike this year, oil says he should, AI says he should be cutting aggressively — and hike or cut, LONG yields likely rise either way because the long end trades supply, not policy; his read of balance-sheet-reduction talk is 'farcical,' with 'date three' (a dysfunction episode) ending in buying, not shrinking. He self-grades 'no edge' on the meeting itself — weighted accordingly. Changes our mind: job growth turning negative, or oil resolving lower.

HELD at 65 with the release valve showing up first in Japan, not the US. The Bank of Japan and the US Treasury ran a COORDINATED currency intervention of $53B in a single day, the largest ever recorded, after the yen hit a 40-year low near 164 to the dollar; it now trades 157.5. Two things follow. The intervention itself is the thesis in miniature: a G7 government whose debt makes a rate defence unaffordable defends its currency by direct market operation instead, and the Big Mac benchmark (a US Big Mac at $6.22 against 500 yen in Japan implies about 80) says the yen is still roughly 50% undervalued, so this is a first instalment rather than a fix. And the US Treasury participating tells you Washington now treats a disorderly yen as its own problem, because a collapsing yen forces Japanese institutions to sell the Treasuries this thesis needs someone to buy. The honest counterweight, and the reason this stays 65 rather than moving up: the US 10-year REAL yield (the nominal yield minus expected inflation, the true cost of money) sits at 2.41%, the 96th percentile of its recorded history. That is the opposite of the financial repression this thesis assumes, and it is why gold is down about 26% from its February high while still holding the $4,000 line at $4,107. Repression is the destination; it is not the present condition. With interest expense ~$1.4T/year and deficits ~6% of GDP, long Treasury yields can't durably fall even in a recession — the classic "bonds rally in the crash" hedge is broken (Gundlach; Lacy Hunt's capitulation marks the regime as accepted). Endgame: the debt lands on the Fed's balance sheet and the dollar is the release valve. Bullish gold, bitcoin, and stocks measured in dollars. Jeffrey Currie (ex-Goldman commodities head) is outright long gold. The maximalist version of this thesis got a named owner: Russell Clark (ex-Horseman Capital) targets a 10% 10-year Treasury yield — his mechanism is political regime change (pro-labor, full-employment politics replacing the post-1980 pro-capital order; 1970s rates hit 15-20% with debt-to-GDP under 20%, so sustainability arithmetic is not the constraint, wage politics is) plus foreign-reserve demand reverting from sovereign bonds to gold since the 2022 Russian reserve freeze; his supporting tell is private credit — the Cliffwater fund gated redemptions as subscriptions were outrun for the first time — logged as a heavy-bear bonds NEW VIEW, kept as the tail beyond Gundlach's 4.6% fair-value anchor, not averaged into it. The mechanism of the moment is Boockvar's: markets "choking on excess supply for the first time in my lifetime" (hyperscaler AI debt plus global defense budgets) pushes REAL rates up — gold's classic headwind, temporary in his view; he buys the pullback and sells the dollar (a 97→101 rally against 1.5 newly-priced hikes is "not much of a rally"). Gold at $4,121 is HOLDING the reclaimed $4,000 zone — the add-gate row is TRIGGERED, the add-zone open while it holds — but the correction now has a dated map: Benjamin Cowen's midterm-year template puts gold's low between July and October with the bull-market support band near $3,800 (~4% below) likely tagged first; prior midterm years bottomed -10 to -11% from the yearly open versus -5 to -6% now, and silver keeps bleeding versus gold until gold's low is in. His end-of-decade bull case sits on the far side of that low. The tactical picture flipped a name Thursday: Ceresna — "the bull trend is just not your friend yet" only a week ago — put on the roster's first defined-risk lean-in, long GLD near $376 wrapped in a September collar (downside protection from $370 to $350, upside capped at $415, $1.75 per share net cost), arguing the six-month, 30% correction has cleared most of the excess while positioning shows nobody left (large specs still near half the market, small specs unchanged through the whole drawdown — sticky hands, potential fuel); he still flags that a failed rally back to $4,000 opens the $3,800 retest. Kevin Wadsworth (Northstar, chartist) holds the evidence gate on the other side, first-hand as of his July 18 roundup: "nothing on the chart yet to say that the correction is over" — basing expected $3,700-4,000, with $3,760 then the rising three-year average near $3,126 as the supports below, and new adds requiring a base plus a reclaim of the $4,300 area; his discipline costs money by design — the confirming evidence "will come at a higher price point." Silver is the weaker metal on his screen: retesting the $55-57 breakout, low-to-mid $40s if it fails. DoubleLine's desk would turn bullish at $3,700-3,800. The CEF top-up stays suspended pending either the $4,300 reclaim or a decisive weekly close below $4,000 — both rows now on the trigger board. Central-bank gold accumulation over Treasuries remains the global trend (Dixon, Thornton, Alden). The level gates the add, not the thesis. HIGH-WEIGHT UPDATE (2026-07-29, Ian's directive): Gromen's full YCC framework ingested and claim-checked (transcripts/2026-07-29_gromen_other-peoples-money_ycc.md; adjudication in memos/2026-07-29_gromen_highweight.md). The verified legs move the number 63→65: interest + entitlements + veterans benefits run ~100%+ of receipts (arithmetic checks against FY25-26 budget data; VA alone $400B+), the Fed's own Oct-2025 note confirms the basis-trade/Cayman complex as the fragile marginal buyer (~$1.4T of obscured holdings; monthly-mandate leverage that de-grosses on any vol spike — why long yields now RISE on risk-off, 'very fickle creditors'), and the historic creditor bloc (Japan, Germany, Korea, UK) is running defense stimmies — competing SELLERS of duration now, not buyers. His endgame specificity becomes the thesis's mechanism: de facto YCC arriving under a 'market functioning' alias after a dysfunction episode, dollar devalued (particularly against gold) until debt/GDP lands ~60-80%; high real yields are ruled out because they kill the debt-financed AI capex that IS current US growth. Signposts join the board: oil >$85 opens the Treasury-dysfunction band (new row wti_85_dysfunction; 60-80 is the safe band), the 10y 4.7% war-affordability line (row y10_470 already live), and any G7 bond-buying announced 'for market functioning' = YCC under an alias → Phase 3 executes. Discipline notes kept: his China gold tonnage (173t June) is NOT verified — official PBoC printed ~15t; direction confirmed, magnitude carried as unofficial estimate. His dated gold path ($5,000 in a year, $10,000 in five; S&P up in dollars, down in gold) is logged for grading, not adopted as a gate. Imposed falsifier (he offers none): a smooth UST auction cycle with term premium FALLING while oil holds >$85 weakens the dysfunction leg. DOLLAR LEG GATED (2026-07-31, Ian's directive): this thesis says the dollar takes the hit, but until now it was the only structural call on the board with no level to grade it against, which is why the leg could sit "pending" indefinitely. Gates set: broad dollar below 117.45 (the June low) CONFIRMS the leg and opens an explicit FX expression for review; above 122.70 holds the FX expression closed and says the debasement is being paid in gold and bitcoin only. Between them (now 120.71, +2.8% off the low after four months of 117.5-122.7 chop) no FX action either way. The reason the book is short the dollar's purchasing power and not its exchange rate is arithmetic, not caution: over the same window the broad dollar fell 2.9% while gold rose 69%, and shorting a currency whose front end prices hikes (2-year 63bp above funds) is negative carry into a headwind. Roster discipline note: the dollar bears and dollar bulls are on different clocks, not in conflict - since Jul 1 the stance ledger runs 16 bearish / 9 bullish / 1 neutral, averaging -0.5, and splits by horizon into secular -1.38 (n=8), cycle -0.86 (n=7), short-horizon +0.5 (n=10). Do not render that as a consensus. Changes our mind: a credible deficit-reduction path, or central banks turning from gold buyers to sellers.

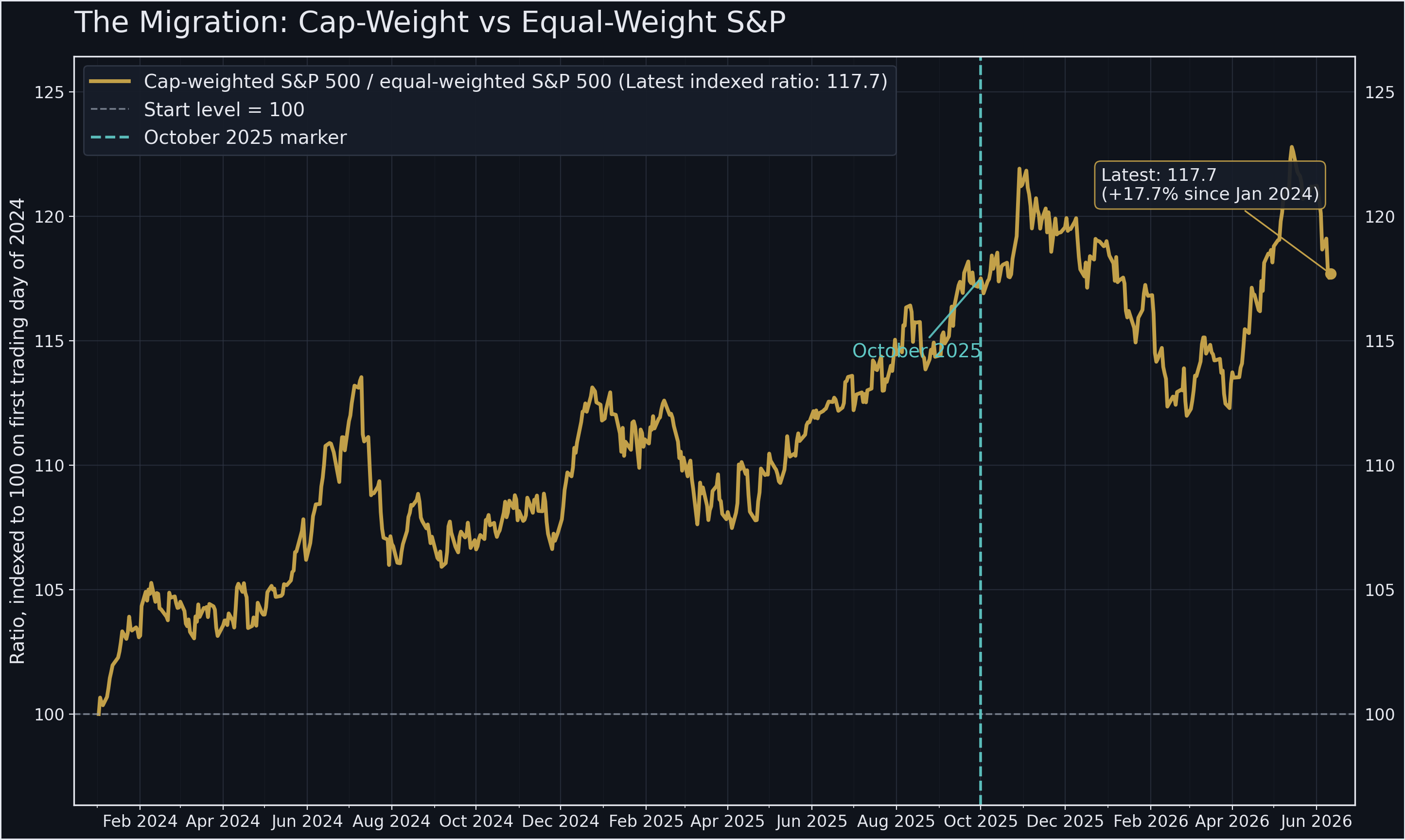

RAISED 70→72 because the migration stopped being a forecast and became the scoreboard. The equal-weight S&P 500 (which holds every constituent at the same size, so it measures the average stock rather than the giants) is now up 13.5% year to date against 10% for the standard cap-weighted index — the rotation has TAKEN the lead, not merely narrowed the gap. July's internals are the mechanism: Morgan Stanley's long-momentum basket fell 19% on the month while its short-momentum basket rose 7.5%, a 25-point performance gap inside four weeks; technology fell 8% month to date while energy rose 11-15% and consumer discretionary was the best sector on the week at +6% (DoubleLine desk). Named dissent, and it is the strongest counter this thesis has faced: Goldman Sachs Wealth Management RAISED its 2026 S&P 500 earnings growth forecast mid-year from about 10% to about 17%, with the non-Mag-7 remainder — the other 493 companies and the median stock — growing 10-12% against a post-war trend of 6.5%. If that holds, the broadening is earnings-driven health rather than a topping process, and DoubleLine's desk agrees it "points to a healthier stock market." Friday itself ran the other way and is worth logging as the reversal risk: the cap-weighted S&P rose 0.72% to 7,489 while equal-weight fell 0.17% and the Russell 2000 small-cap index fell 0.50%, with the volatility index down to 15.99 — one session of the giants leading again. Prior raise 67→68: the migration is now a flows fact, not a forecast. Tech, media and telecom are a record 49% of the S&P 500 (9 points above the 2000 peak); margin debt hit a record $1.5T (+49% y/y); insiders sold $77.6B against $6.9B bought in H1 (11-to-1); XLK bled $8.7B in a month while financials and healthcare took inflows (Kobeissi). The top five US banks grew Q2 EPS 39% on 20% revenue growth while the equal-weight index absorbed SOX -17% on the month. Valuations sit above the 2000 and 2021 peaks as ~$3.6T of new stock supply drains the crowded index toward small caps, value, and ex-US. New named defection: Luke Gromen turned outright bearish US equities on the debt-adjusted Buffett indicator. Raised 68→70 Thursday afternoon on a defection at the crowd's widest point: Patrick Ceresna (Macro Voices — the same desk that mapped the CTA triggers) flipped from lean-bull to lean-bear inside six days: "the market right now is quite vulnerable." His mechanism is mechanical, not narrative: after weeks of sideways tape, trend-following funds' flip points have risen underneath the market like a trailing stop, so even a 150-200-point S&P drop starts forced systematic selling with 7,000 the air pocket below. The crowd he left got broader as he exited — large AND small speculators both sit at 90 out of 100 on their one-year positioning scores (CFTC commitment-of-traders data via Macro Voices), with small specs' pile-in the single biggest positioning jump on the board — and uniform crowding amplifies any downside catalyst. The line was tested the same day he flagged it: the S&P touched the ~7,400 CTA shelf at Thursday noon (7,402, with Tesla -14% doing the pulling) and held, back to ~7,413 by early afternoon; first test passed, VIX 19.2. The tactical counter DEFECTED July 30: Gundlach's "rise period" constructive of last week flipped to "passive investing is a trap right now — a momentum trap" (a stance-ledger sign flip, the strongest trade-with class): passive equity money now exceeds active, and shortened lockups plus accelerated index inclusion (SpaceX the live case) let insiders exit into the price-insensitive passive bid — his prescription stays equal-weight, which "will continue" to work; with Cowen's dated correction, Rooney Vera's correction-underway call and James's trend-turn all landing the same week, the short-term bear side is now the CROWDED side — the contrarian caution cuts against the correction camp for the first time; Wadsworth's chart adds a second shelf below Ceresna's — above ~7,300 the melt-up toward 8,000-9,000 stays alive, below it "something else is going on" — while his Straits Times extension gauge sits at the same extremes that preceded the 1999 and 2007 busts. The correction case has a date and a trigger: Cowen's midterm template (2014, 2018, 2022 — three for three) calls for a 10-20% decline topping in August-September with elevated semiconductors the likely spark; against it, Visser's no-recession checklist (S&P earnings strongly positive year-over-year, junk spreads near record tights, no claims deterioration) says rotation keeps absorbing the damage. WSJ reports everyday investors souring on the Mag Seven and rotating to newer AI trades — the migration reaching retail. Expression complication: ISRG broke its 200-week floor after a clean beat — stabilize this week or be rethought. Changes our mind: the S&P breaks support (rotation becomes bear market), or the giants reclaim leadership.